- What is Credit Card Fraud?

- 7 Steps to Recover from Credit Card Fraud

- Signs of Credit Card Fraud

- Tips to Protect Yourself Against Credit Card Fraud

- Frequently Asked Questions

Credit card fraud is on the rise. Despite the security measures that credit card providers develop to prevent unauthorized card usage, scammers are becoming ever-more resourceful at working around these methods.

Dealing with credit card fraud can cost you a lot of time and worry, and although federal law limits your liability to $50, the cost of the theft adds to the overall cost of using credit cards—in interest rates and fees—for all account holders.

Follow the proper steps after a lost or stolen credit card and not only will you save yourself a lot of aggravation, but also limit the damage to your credit report.

What is Credit Card Fraud?

Credit card fraud is a form of identity theft where scammers make unauthorized purchases or withdrawals using your card. This can occur via the theft of your physical card or by stealing your account numbers and PINs. Types of credit card fraud include:

- Card theft: When your card is stolen, or a newly issued card is swiped from your mailbox.

- Cloned cards: Scammers use devices called “skimmers” that fit over card readers on ATMs or card readers that steal your card numbers when you swipe your card. They then make a duplicate of your card for illicit use.

- Account hijacking: Scammers contact your card issuer and use your personal data (stolen through phishing or by trawling social media) to take over your account and block you out. If you don’t use your credit card that often, it may take a while to detect the fraud.

- Stolen card number: This kind of credit card fraud doesn’t require possession of a physical card. More commonly used for unauthorized online purchases, the scammer typically only needs your name, credit card number, the card’s security code, and your zip code. Scammers can get hold of this information through data breaches of card-number databases.

7 Steps to Recover from Credit Card Fraud

If your credit card has been lost or stolen, or you suspect you’re a victim of credit card fraud, acting fast is critical to mitigating your damages. As soon as you discover your card is missing, or detect suspicious activity on your account, follow our step-by-step guide.

1. Cancel Your Credit Cards

Notify your credit card provider immediately that your card is lost or stolen. You’ll be able to put a block on your card to prevent the scammer from placing too many unauthorized charges on your card.

Thankfully, federal law limits your liability to $50 if you’re the victim of credit card fraud, but if you act fast and resolve the matter before there are unauthorized charges, you won’t be liable for anything.

Your credit card will be canceled, and a new one will be issued to you in the mail with a new account number. Don’t worry; having a card replaced shouldn’t affect your credit score.

What You’ll Need

Your credit card provider will need to verify your identity thoroughly, particularly if a scammer has taken over your credit card account. You’ll need your name, address, Social Security number, and potentially other information about your account.

You’ll also need to know when the last legitimate transaction was, so your credit card provider can identify if there have been any fraudulent transactions, withdrawals, or if your card has been used to set up unauthorized direct debits.

2. Dispute Any Fraudulent Transactions

Check your credit card statement for fraudulent transactions and let your card issuer know that these were not yours. Many banks allow you to dispute transactions easily online by logging into your account (including via your bank’s mobile app).

Many banks will refund you the full amount following credit card fraud.

3. Continue to Monitor Your Credit Card Statements

After you’ve reported your card lost or stolen, keep a close eye on your credit card statement for any further incidences of fraudulent activity. Just because you've canceled your card, it doesn't mean the scammer doesn't have your login information or another way to steal your money.

If you spot anything suspicious or unfamiliar, call your credit card provider as soon as possible.

4. Check Your Credit Reports

If you’re the victim of credit card fraud, you could become the victim of other forms of identity theft. Therefore, it’s a good idea to check your credit reports to see if new lines of credit have been opened in your name without your permission.

Free Credit Reports

You can claim a free copy of all three of your credit reports from AnnualCreditReport.com once a year.

If you find anything suspicious, put a freeze on your credit. This will prevent any more lines of credit from being opened in your name. If you don’t want to put a complete freeze on your accounts, you can place a fraud alert which will require creditors to confirm your identity first.

Recovering from identity theft can take years, so you must act quickly and continue to monitor your credit reports.

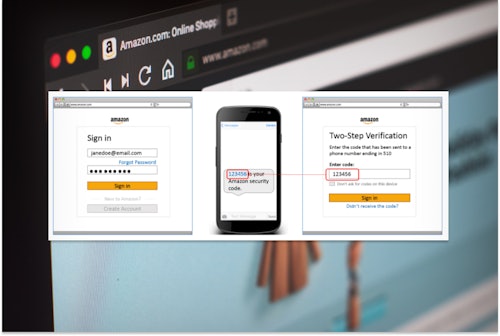

5. Change Your Account Passwords

After any form of identity theft, you should change your account passwords in case a scammer has hacked your device. If you suspect this is the case, use a different computer to change your password, as a scammer may be logging your keystrokes. In addition, you’ll need to change your credit card account password and any other logins that use the same password.

Use a password manager to generate unique and strong passwords for your financial and other online accounts. Additionally, make sure your security and operating software are up to date to protect you from any further cyberattacks.

6. Check Your Insurance Coverage

It is always worth checking your homeowner’s or renter’s insurance to see if you’re covered for credit card theft. Although your liability for credit card fraud is limited to $50, your insurance may cover this cost so that you won’t have out-of-pocket expenses.

Even better, some credit card providers offer zero liability for fraud as an account feature, which is something to consider if you’re looking to switch cards.

7. Report the Credit Card Fraud to the Authorities

Report the credit card fraud to the Federal Trade Commission (FTC). You can do this easily online, and you’ll be issued an Identity Theft Report that will act as proof that you’re a victim of identity theft. In addition, this report will help you fix your credit reports and remove unauthorized accounts.

You may also want to file a report with your local police department using your Identity Theft Report. Doing so can help investigate theft and fraud and protect you and others from further damages.

Signs of Credit Card Fraud

There are a few warning signs that may indicate that you’re a victim of credit card fraud. They include:

- A rejected credit card when you try to make a transaction or a withdrawal (even when you know you still have credit available).

- Exceeding your credit limit despite knowing you haven’t done that much spending on your card.

- Unusual transactions on your bank statements from vendors you don’t recognize and purchases you don’t remember.

- Changes to your account details that you haven’t requested.

Tips to Protect Yourself Against Credit Card Fraud

Lower your risk of credit card fraud by following our top tips:

- Check your credit card statements as soon as they arrive, and make sure you can account for all transactions and withdrawals. Shred paper copies of your statements once you’ve checked them.

- Keep your account number safe. Scammers don’t always need your physical card to commit credit card fraud. Your account number may be enough, so be careful not to write it down anywhere someone may find it.

- Shield your PIN when entering it into an ATM or payment reader, and always keep your pin private and not something easy to guess, like your date of birth. Plus, if an ATM looks like it’s been tampered with, don’t put your credit card in and report it to your bank.

- Never share your credit card number over the phone with an unsolicited caller, even if they claim to be from your bank.

- Only use trusted platforms and secure websites when shopping online, with HTTPS or the padlock symbol at the left side of the browser bar. Plus, always log out of your vendor account after you’ve completed your purchase.

- Ensure your security software is up to date on all your devices and run regular virus scans to check for malware that could have been placed there by scammers.

- Don’t let websites save your credit card details for future use, and always avoid entering your card details when connecting to public WiFi or shared computers.

- Check whether your data has been compromised when you hear about a data breach on the news and fear you may be affected. You can use services like Have I Been Pwned to monitor data breaches linked to your email account.

- Check for credit card skimmers, especially at gas stations and convenience stores located in quiet or more sketchy parts of town.

How to Keep Your Physical Credit Card Safe

- Only carry the cards you need.

- Keep your cards in a secure wallet or purse, not just in your pocket.

- Store your unused cards in a secure place and keep track of the ones you do use.

- Cut up old cards before you through them away, being sure to cut through the account number, magnetic stripe, and chip.

Comments